🎧 Listen to the Audio Version of This Article

Introduction

Financial scams rarely begin by looking like scams. If they did, almost no one would fall for them. They usually appear as an opportunity, a referral, an exclusive investment, a limited chance, a simple business, extra income, or an invitation from someone who seems trustworthy.

That is why, when someone loses money to fraud, the most common explanation is often the most unfair one: “they were greedy,” “they were naive,” “they lacked intelligence.” That answer may sound simple, but it ignores almost everything that makes financial scams effective.

In practice, a well-built scam does not depend only on an uninformed victim. It depends on a favorable psychological environment. The scammer is not merely selling an investment, a course, a digital currency, a business opportunity, or a promise of profit. He is selling relief, urgency, belonging, hope, status, fear of being left behind, and the feeling that a way out has finally appeared.

This matters because many people who fall for scams are not careless in every area of life. Some work, study, manage families, make complex decisions, and are seen as responsible. Even so, at a certain moment, facing a certain promise and inside a certain emotional state, they end up believing.

The central question is not only “how could someone believe this?” A more useful question is different: which emotional needs, mental shortcuts, and social pressures made that offer seem reasonable at the moment it was presented?

Understanding this does not remove responsibility from the person who deceives. On the contrary. It helps explain why certain mechanisms of manipulation work and why anyone can become vulnerable when a promise speaks directly to a pain, an ambition, or a specific fragility.

Financial scams exploit the mind before they exploit the bank account. They enter through trust, pressure, the desire for a better life, comparison with others, and the difficulty of admitting doubt when everyone around seems convinced. That is why studying this topic is not only a matter of finance. It is a matter of practical psychology.

Summary

- A Financial Scam Does Not Begin With Money, It Begins With Need

- The Promise of Fast Money and the Mental Shortcut of Hope

- Authority, Social Proof, and the Desire to Belong

- The Role of Urgency, Fear, and Psychological Pressure

- Why Intelligent People Also Fall for Scams

- How to Recognize the Psychological Signs of a Financial Scam

- Conclusion

A Financial Scam Does Not Begin With Money, It Begins With Need

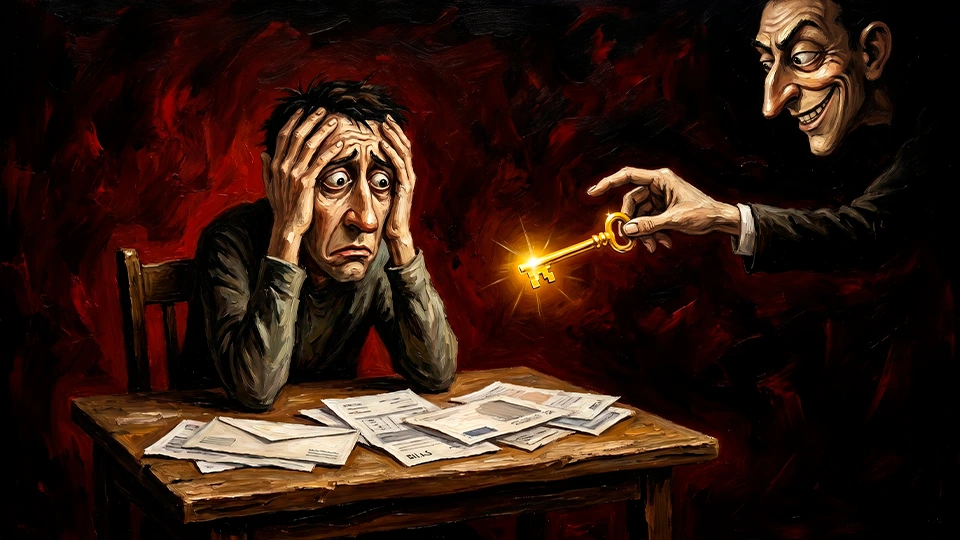

A financial scam becomes more convincing when it meets a real need. It may be the need to pay debts, help family, recover losses, improve one’s life, prove competence, escape a difficult phase, or simply feel that there is still a chance to turn things around.

Money, in this context, is not just money. It represents security, freedom, recognition, peace of mind, and control over the future. When someone is emotionally pressured, a financial promise can feel like more than an opportunity: it can feel like an answer.

This is one reason many frauds are presented as simple solutions to complex problems. The scammer understands that a person tired of financial instability may be more open to an offer that promises quick results. Not because that person cannot think, but because the offer appears exactly where suffering is asking for relief.

There is also an important difference between desire and vulnerability. Wanting to earn money does not automatically make someone vulnerable. The problem begins when that desire combines with emotional urgency. A person in debt may not evaluate a promise the same way they would in a stable moment. Someone who recently lost money may cling to the idea of recovering everything quickly. Someone who feels behind in life may interpret a risky invitation as the last chance to catch up.

The scammer rarely needs to convince the person of something completely new. Often, he simply gives shape to a hope that already existed. He offers a narrative that seems to organize the victim’s frustration: “you did not fail, you just did not know the right method”; “you worked hard, but you were in the wrong system”; “wealthy people know this and do not tell anyone”; “this opportunity came to only a few people.”

Those phrases do not work only because they promise money. They work because they offer an emotional explanation for the person’s pain. And an explanation that preserves self-esteem is often more attractive than a cold analysis of risk.

That is why the first psychological layer of financial scams is need. When the promise touches a wound, the mind may start looking for reasons to believe instead of looking for reasons to be cautious.

The Promise of Fast Money and the Mental Shortcut of Hope

The idea of making money quickly is seductive because it offers a break from the slowness of real life. Working, saving, studying, investing prudently, building assets, and improving one’s financial condition usually take time. The scam offers the opposite: a short, direct path that seems reserved for those brave enough to act before everyone else.

Psychologically, that promise activates a powerful mental shortcut. The human mind does not always calculate risk with cold precision. Often, it calculates possibilities based on the emotional impact of the desired outcome. If the imagined reward feels large enough, the person may begin to minimize danger signals.

This is where phrases appear: “what if it is true?”, “I will put in just a little,” “I know people who made money,” “maybe I am being too fearful,” “if I do not try, I may regret it.” The decision is no longer evaluated only by what can go wrong. It becomes influenced by the fear of missing an opportunity.

This mechanism is common in scams that promise very high returns with little risk. Investor protection authorities often warn that promises of high, consistent, and almost guaranteed returns are classic signs of fraud. But in the moment of decision, the person does not always interpret that promise as a warning. Sometimes, they interpret it as an exception.

The scammer knows how to exploit this opening. He presents the opportunity as rare, exclusive, or misunderstood by most people. Suspicion stops looking like prudence and starts looking like lack of vision. The person who questions is treated as someone trapped in ordinary thinking. The person who believes feels smarter, bolder, or more alert to opportunities others cannot see.

This inversion is central. The scam does not only promise profit. It offers identity. The person is not merely investing; they are seeing themselves as someone who finally understood a hidden logic. And when a financial decision begins to protect an identity, it becomes harder to question.

Hope, in this case, is not the problem. Hope is necessary for action, planning, and building. The problem begins when hope is separated from verification. Healthy hope accepts questions. Manipulated hope demands blind faith, speed, and silence in the face of doubt.

Authority, Social Proof, and the Desire to Belong

Few people like to admit they are influenced by the group. Even so, social proof is one of the strongest forces in human decision-making. When many people seem to believe something, it tends to feel safer. When someone who appears authoritative recommends something, resistance decreases.

Financial scams exploit exactly this. They use testimonials, screenshots, messaging groups, influencers, supposed specialists, luxury images, technical language, rankings, events, mentorships, and closed communities to create a feeling of legitimacy. The implied message is simple: “it is not just you; many people are already in.”

That feeling reduces the discomfort of doubt. If other people are investing, maybe it is real. If someone shows gains, maybe it works. If the group celebrates results, maybe the risk is lower. If the leader speaks confidently, maybe he knows something others do not.

The problem is that fraudulent environments can manufacture trust. Testimonials can be false. Results can be selectively shown. Screenshots can be manipulated. Real people may receive small initial payments only to build credibility. An entire group can work like a stage, where each message reinforces the impression that everyone is winning.

There is also the desire to belong. Joining an opportunity may mean becoming part of a community, feeling chosen, talking to people who seem ambitious, and escaping the feeling of standing still. For someone who feels alone, behind, or undervalued, that belonging may weigh more than the technical details of the offer.

There is another delicate factor: when the recommendation comes from someone familiar, defenses drop. Many frauds spread through networks of trust. A friend invites another friend. A relative calls another relative. A colleague shares their own experience. In many cases, the person who recommends the scheme also believes they are helping. This makes the scam even more confusing, because the victim does not feel they are dealing with a distant criminal, but with someone close who seems convinced.

This is important: social trust does not replace verification. The fact that someone you know believes something does not make it safe. They may have been deceived first. They may have received an early return. They may be trying to recover money by bringing in new participants. They may simply not understand the risk.

When social proof enters the scene, the most important question is no longer “who is doing it?” but “what proves that this is legitimate, regulated, transparent, and sustainable?”

The Role of Urgency, Fear, and Psychological Pressure

Financial scams almost always involve pressure. The opportunity ends today. Spots are limited. The price will rise. The group will close. Those who enter now get the best phase. Those who wait lose. This urgency is not a detail; it is a control technique.

When a person feels they must decide quickly, their capacity for analysis decreases. Pressure moves the mind away from rational examination and toward emotional reaction. Instead of investigating, the person tries not to miss out. Instead of comparing information, they seek immediate reassurance. Instead of talking to someone neutral, they listen only to the person pushing the decision.

The fear of missing a chance can be as strong as the desire to earn money. In many scams, the pressure does not come only from the promise of profit, but from the psychological threat of exclusion. The person begins to imagine that, if they do not enter, they will watch everyone around them prosper while they remain in the same place.

This fear is intensified when the scam presents itself as an opportunity that “will not come back.” The mind begins to treat the decision as if it were facing a single door. Under that condition, doubt feels dangerous, because doubting may mean being left out.

Another common tactic is isolation. The scammer discourages the victim from seeking outside opinions. He may say that family members would not understand, that banks and traditional institutions have an interest in hiding opportunities, that negative people always criticize, or that those who ask too many questions never prosper. The victim is surrounded by a narrative that turns prudence into weakness.

This manipulation is especially effective because many people already carry frustrations with the traditional financial system. Fees, bureaucracy, low income, difficulty accessing credit, and a sense of unfairness make the idea of an alternative path more attractive. The scammer presents himself as someone revealing a way out of a system that supposedly wants to keep everyone trapped.

Urgency also blocks a simple question: if the opportunity is so solid, why must it be accepted immediately? Good investments may involve timing, but they should not depend on emotional pressure, absolute secrecy, and the inability to analyze.

When a financial decision does not allow pause, verification, and comparison, the pressure itself is already part of the problem.

Why Intelligent People Also Fall for Scams

One of the most dangerous beliefs about financial scams is the idea that only naive people fall for them. That belief gives a false sense of protection. If I consider myself intelligent, I may think I am immune. But intelligence does not remove emotion, need, pride, fear, the desire to belong, or overconfidence.

Intelligent people can fall for scams precisely because they know how to build sophisticated justifications for bad decisions. They may tell themselves they understood the opportunity better than others, that the risk is calculated, that criticism comes from overly conservative people, or that strange signs are simply part of an innovation the market has not yet understood.

This resembles confirmation bias: once someone starts wanting something to be true, they begin looking for information that confirms that belief and rejecting contrary signs. The person watches positive testimonials, reads favorable comments, follows displayed gains, and avoids critical content. Gradually, they are no longer evaluating the opportunity; they are defending a choice.

Another factor is progressive commitment. Many scams do not ask for a large amount at the beginning. They start small. The person tests it, receives some return, gains confidence, and increases the amount. Later, when problems appear, they have already invested money, time, hope, and identity. Admitting the scam begins to hurt more than continuing to believe.

This is a fundamental psychological point: sometimes the person does not continue because they are still convinced. They continue because stopping would mean facing the loss. The mind tries to protect self-esteem by postponing the conclusion. “Maybe it is just a delay”; “maybe I need to wait”; “maybe I can recover”; “maybe I should deposit more to release the withdrawal.”

Scams exploit this difficulty in accepting losses. They ask for new fees, new deposits, new unlocking steps, new invitations. The victim is no longer seeking profit; they are trying to escape without admitting they were deceived.

There is also shame. When the person begins to suspect something, they may avoid asking for help because they fear judgment. This prolongs the problem. The scam grows in silence, because shame isolates the victim and protects the scammer.

This isolation also harms the memory of the decision. After some time, the person begins to mentally reconstruct the path that led them there and may feel they “should have noticed.” But that later reading is clearer because the signs are now organized by the outcome. At the moment of decision, the signs were mixed with hope, pressure, testimonials, promises, and small confirmations. This is why prevention must happen before emotional capture, not only after the loss.

Intelligent people may also trust too much in their ability to leave in time. In some scams, the victim notices there is risk, but believes they can take advantage of the early phase and withdraw before collapse. That reasoning may look strategic, but it often ignores that real control is in the hands of whoever operates the scheme. Withdrawals may be blocked, rules may change, new fees may appear, and communication may disappear exactly when the victim decides to leave.

That is why a more useful approach is not to humiliate those who fell for a scam, but to understand the mechanisms involved. Moral judgment closes the conversation. Understanding creates room for prevention.

How to Recognize the Psychological Signs of a Financial Scam

Recognizing financial scams does not depend only on knowing mathematics or finance. It also depends on noticing the emotional state the offer produces. A legitimate opportunity can be analyzed calmly. A scam usually stirs urgency, euphoria, fear, secrecy, or a feeling of privilege.

Some signs deserve special attention:

- a promise of high returns with little or no risk;

- guaranteed or constant profit, regardless of the market;

- pressure to decide quickly;

- an invitation coming through an unexpected message, closed group, or hard-to-verify contact;

- difficulty understanding exactly how the money is generated;

- technical explanations that impress more than they clarify;

- demands for new payments to release withdrawals;

- encouragement to invite other people;

- discrediting anyone who asks questions;

- lack of registration, clear contracts, supervision, or transparency.

Beyond those external signs, there are internal signs. If the offer makes you feel that you must act before thinking, stop. If you feel afraid to ask someone outside the group, stop. If the thought of missing the opportunity feels unbearable, stop. If you notice that you are looking only for favorable information, stop.

A good psychological rule is to create distance between emotion and decision. Never make important financial decisions at the peak of excitement, fear, or desperation. Wait. Research. Talk to someone who has no interest in your participation. Verify registrations, companies, responsible parties, risks, contracts, and official channels. If the opportunity is legitimate, it will withstand questions.

It is also important to distrust offers that attack prudence. When someone says that “people who think too much never get rich,” they may be trying to block exactly what could protect you. Thinking, asking, and verifying are not signs of weakness. They are defense mechanisms.

Another important care is separating desire from evidence. Wanting something to be true does not make it true. Knowing someone who made money does not prove sustainability. Seeing screenshots does not prove legitimacy. Being part of an excited group does not prove safety. A financial decision needs more than collective enthusiasm.

In the end, the best protection is not distrusting everything. It is learning to distrust your own emotional state when a promise feels too perfect to be examined.

Conclusion

Some people believe financial scams because scams do not attack reason alone. They attack needs, hopes, fears, social bonds, pride, comparison, and the desire for change. An effective scam does not feel absurd to someone inside the narrative. It feels like an opportunity that finally makes sense.

That is why prevention must go beyond saying “research before investing.” Research is essential, but many people do not research because they have already been emotionally captured. Before fraud takes the money, it takes interpretation. It makes prudence look like fear, doubt look like negativity, and pressure look like courage.

Understanding the psychology of financial scams helps recover a more lucid posture. No serious opportunity should demand blind faith, secrecy, artificial urgency, or distance from outside opinions. No promise of profit should avoid clear explanation about risk, the source of return, and the possibility of loss.

Intelligent, hardworking, careful people can also be deceived. This should not create paranoia, but humility. The humility to recognize that all of us have vulnerable points. The humility to pause when something stirs too much hope. The humility to ask for a second opinion before turning desire into decision.

Deep down, the question is not only “why do some people believe financial scams?” The deeper question is: what part of us wants so much to believe in a quick way out that, for a few moments, it stops hearing the warning signs?

Answering that question may be one of the most important forms of protection. Because a mind that understands its own vulnerability becomes less available for manipulation. And in a world where financial promises appear increasingly well packaged, that awareness may be worth far more than any promise of easy profit.

Institutional sources consulted to support the warning signs discussed:

Investor.gov sobre esquemas Ponzi, Investor.gov sobre como evitar fraudes e FTC Consumer Advice sobre golpes.